The Annual Information Statement (AIS), initiated by the Income Tax Department to improve transparency, is unfortunately causing challenges for taxpayers by reporting inaccurate income figures, according to chartered accountants.

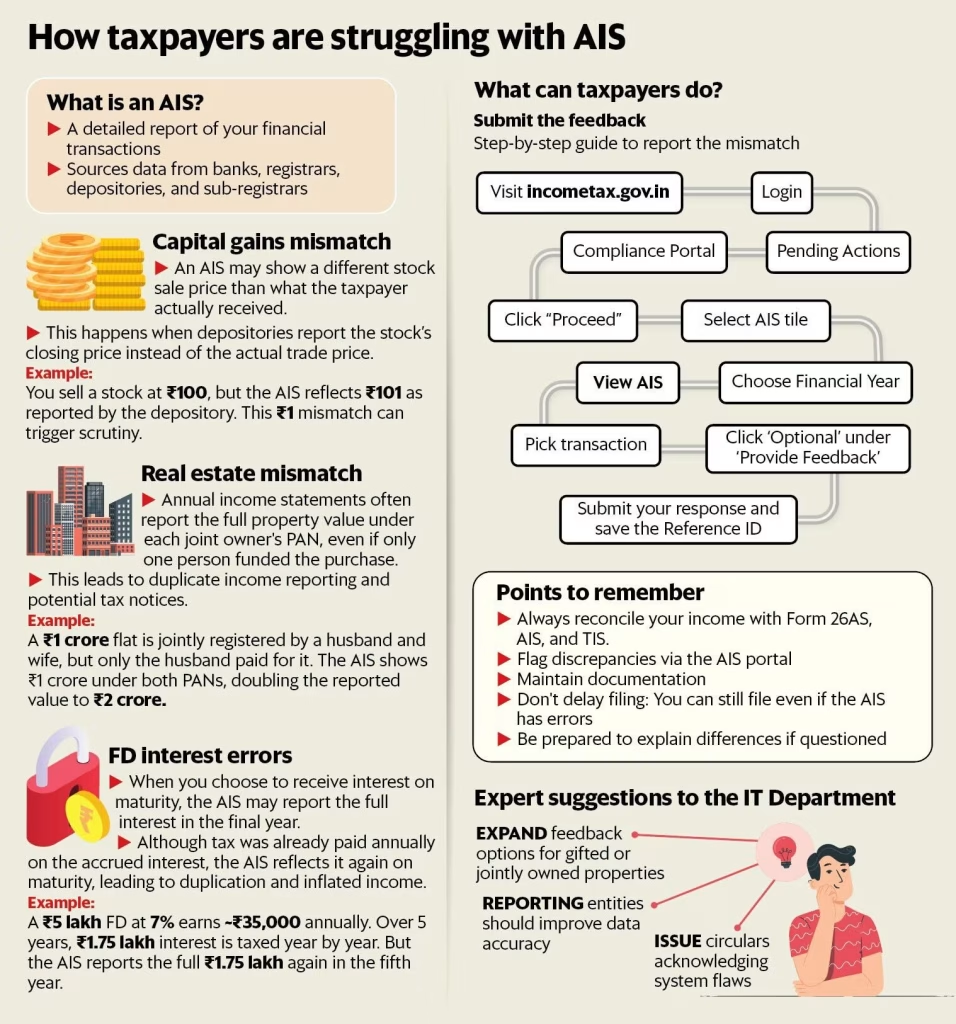

Launched in 2021, the AIS provides a comprehensive view of financial activities—from securities and mutual fund transactions to real estate purchases and fixed deposits—over a fiscal year, compiled from various reporting sources such as banks, registrars, depositories, and sub-registrars.

Accessible via the Income Tax e-Filing portal, the AIS complements Form 26AS by delivering an enriched perspective of different income sources and transactions that could have tax consequences.

However, it is frequently plagued by inaccuracies that expose taxpayers to the risk of notices and assessments.

Challenges Faced

A prevalent issue within the AIS involves capital market transactions, particularly in equity trading. While brokers and depositories provide trade information, there are often discrepancies between reported prices and actual trade values.

“We have encountered numerous significant mismatches in tax declarations that can pose serious issues for taxpayers. For example, in equity deals, depositories oftentimes report closing prices that differ slightly from the actual transaction prices,” stated Ashish Karundia, a chartered accountant and founder of Ashish Karundia & Co.

These inconsistencies often stem from systems that fail to capture real-time transaction prices or details specific to settlements.

“I have handled cases involving senior citizens who do not even possess a demat account, yet the AIS inaccurately recorded capital gains for them. These individuals have never engaged in any security transactions throughout their lives, but the system indicated otherwise,” remarked lawyer and chartered accountant Kinjal Bhuta, who is also a treasurer at the Bombay Chartered Accountants’ Society.

Property transactions represent another significant source of confusion in the AIS, particularly when it comes to joint ownership. The system frequently attributes the full property value to each co-owner, leading to inflated income reports.

“One reason for this issue is that real estate, fixed deposits, securities, or mutual fund shares might have been acquired in joint names purely for convenience or as a token gesture. However, the second (joint) owner might not have contributed financially to the purchase,” explained Pankaj Bhuta, chartered accountant and founder of P. R. Bhuta & Co.

The reporting systems commonly double-count the property value, distorting the financial reality of the ownership arrangement.

Even gifting transactions suffer from reporting errors. “We encountered a curious case regarding property gifting. When a gift deed is executed and registered under stamp duty, the system incorrectly classifies it as a sale and purchase. As a result, both the giver and receiver receive notices based on the stamp duty value and fair market value, despite it being merely a gift,” Kinjal Bhuta noted.

This misunderstanding arises from how sub-registrars log transactions, pointed out Ganesh Rajgopalan, partner at A.P. Rajagopalan & Co.

“When joint property dealings are registered, sub-registrars duplicate the same transaction across each joint owner, creating a convoluted reporting landscape. Thus, a single property transaction can be recorded multiple times for different PAN (Permanent Account Number) holders, lacking clarity regarding the individual ownership stakes,” he stated.

The AIS also tends to misrepresent interest income from fixed deposits. This often occurs when a taxpayer chooses to receive interest at maturity, while still being obliged to pay tax on the interest accrued annually according to the accrual method. In such cases, the AIS may either overlook the yearly interest accrual or exaggerate the income when the maturity happens.

For example, if an individual invests ₹5 lakh in a five-year fixed deposit with a 7% annual interest rate, an interest of about ₹35,000 accrues each year for a total of ₹1.75 lakh over five years. Ideally, this interest should be reported annually and taxed accordingly. However, if the bank only reports the total maturity value of ₹6.75 lakh (principal + interest) in the final year, the AIS may inaccurately attribute the entire ₹1.75 lakh interest as income in that year, inflating the reported income.

What Can Taxpayers Do?

If you identify discrepancies in your AIS, your first action should be to reconcile the data—comparing the AIS, Form 26AS, and Taxpayer Information Summary (TIS) with your own records.

“Always verify your income against Form 26AS, AIS, and TIS. If you discover any inconsistencies, you can express your disagreement through the AIS portal on the Income Tax Department website. Be sure to keep all supporting documents to back up your claims,” advised Pankaj Bhuta.

He outlines a simple process:

- Log in to Income Tax Portal

- Navigate to Pending Actions → Compliance Portal

- Click “Proceed” and select the AIS tile

- Choose the financial year → View AIS → Select the transaction

- Click ‘Optional’ under ‘Provide Feedback’ and submit your response.

Make sure to keep the acknowledgment (Reference ID) for future reference.

Karundia suggested that taxpayers should categorize the type of mismatch, prepare a reconciliation statement, and submit it via the AIS platform. “If the issue is not resolved through the AIS feedback channel, taxpayers might also consider reaching out directly to the reporting entities for corrections.

Recommendations for the Tax Department

The annual information statements currently lack legal grounding. “Taxpayers are permitted to contest these AIS entries since there is no legislation validating these reports. The department has established these procedures without a robust legislative underpinning,” noted Kinjal Bhuta.

She also urged the government to release public clarifications whenever inaccuracies or delays occur.

“There should be an avenue for taxpayers to explain the rationale for including a second/joint name and to submit supporting documents,” added Pankaj Bhuta.

Karundia suggested broadening feedback mechanisms on the AIS platform. “Introducing a process where taxpayers can communicate feedback directly to reporting entities would improve accountability and likely accelerate resolution times.”

“The existing process of addressing queries to sub-registrars is inherently flawed and complicates matters unnecessarily for taxpayers. The Income Tax Department should develop advanced software algorithms to automatically reconcile transaction values,” emphasized Rajgopalan.