1. Income Tax Slab Rate for Individual (resident or non-resident) HUF or AOP or BOI or any other artificial juridical person :

Individual (resident or non-resident), (Other than senior and super senior citizen) (HUF or AOP or BOI whether incorporated or not or every Artificial Juridical Person) (AJP)::

| Net income range | Income-Tax rate | |

| AY 2021-22 | AY 2022-23 | |

| Upto Rs. 2,50,000 | Nil | Nil |

| Rs. 2,50,000 – Rs. 5,00,000 | 5% | 5% |

| Rs. 5,00,000 – Rs. 10,00,000 | 20% | 20% |

| Above Rs. 10,00,000 | 30% | 30% |

Resident senior citizen, i.e., every individual, being a resident in India, who is of the age of 60 years or more but less than 80 years at any time during the previous year:

| Net income range | Income-Tax rate | |

| AY 2021-22 | AY 2022-23 | |

| Upto Rs. 3,00,000 | Nil | Nil |

| Rs. 3,00,000 – Rs. 5,00,000 | 5% | 5% |

| Rs. 5,00,000 – Rs. 10,00,000 | 20% | 20% |

| Above Rs. 10,00,000 | 30% | 30% |

Resident super senior citizen, i.e., every individual, being a resident in India, who is of the age of 80 years or more at any time during the previous year:

| Net income range | Income-Tax rate | |

| AY 2021-22 | AY 2022-23 | |

| Upto Rs. 5,00,000 | Nil | Nil |

| Rs. 5,00,000- Rs.10,00,000 | 20% | 20% |

| Above Rs. 10,00,000 | 30% | 30% |

Hindu Undivided Family (including AOP, BOI and Artificial Juridical Person)

| Net income range | Income-Tax rate | |

| AY 2021-22 | AY 2022-23 | |

| Upto Rs. 2,50,000 | Nil | Nil |

| Rs.2,50,000 to Rs. 5,00,000 | 5% | 5% |

| Rs. 5,00,000 – Rs.10,00,000 | 20% | 20% |

| Above Rs. 10,00,000 | 30% | 30% |

ADD:

In addition to the Income Tax amount calculated, based on the above- mentioned tax slabs, these assessees are required to pay Surcharge and Cess as under-

- Surcharge @ 10% of income tax is applicable where the total income exceeds Rs. 50 lakh and upto Rs.1 Crore.

- Surcharge @ 15% of income tax is applicable where the total income exceeds Rs.1 Crores and upto Rs.2 Crores.

- Surcharge @ 25% of income tax is applicable where the total income exceeds Rs.2 Crores and upto Rs.5 Crores.

- Surcharge @ 37% of income tax is applicable where the total income exceeds Rs. 5 Crores and onwards.

- Health & Education Cess levied at the rate of 4% on the amount of Income-tax plus surcharge.

NOTE:

- For salaried persons (including pensioners) standard deduction of Rs.50,000/- or the amount of salary, whichever is less is allowed. [Sec 16 (ia)]

- For persons receiving family pension deduction of thirty three and one- third percent of such pension or Rs.15,000, whichever is less, is allowed. [Sec 57 (iia)]

- Rebate u/s 87A Rs.12,500 or 100% of income tax, whichever is less, if total income does not exceed Rs.5,00,000(applicable for resident individual) [Sec 87A]

- The enhanced surcharge of 25% and 37% as the case may be is not levied, from income chargeable to tax u/s 111A, 112A and 115AD

2. Special tax Rate for Individual and HUFs (New Personal Income-tax regime) (115BAC)

The Finance Act, 2020, has provided an option to Individuals and HUF for payment of taxes at the following reduced rates from assessment Year 2021-22 and onwards:

| Net income range | Income-Tax rate |

| Upto Rs. 2,50,000 | Nil |

| Rs. 2,50,001 – Rs. 5,00,000 | 5% |

| Rs. 5,00,001- Rs.7,50,000 | 10% |

| Rs.7,50,001- Rs.10,00,000 | 15% |

| Rs.10,00,001- Rs.12,50,000 | 20% |

| Rs.12,50,001- Rs.15,00,000 | 25% |

| Above Rs.15,00,000 | 30% |

ADD:

In addition to the Income Tax amount calculated, based on the above- mentioned tax slabs, these assessees are required to pay Surcharge and Cess as given in para 1.5 above.

NOTE:

The option to pay tax at lower rates shall be available only if the total income of assessee is computed without claiming specified exemptions or deductions.

3. Partnership Firm/ LLP

A firm (including LLP) is taxable @ 30 %* for AY 2021-22 and AY 2022-23

* Surcharge @12% of such tax, where the total income exceeds Rs.1 crore.

NOTE:

Subject to marginal relief*.

Health & Education Cess at rate of 4% on amount of Income-tax plus surcharge

* Marginal Relief –

Marginal relief will be provided to certain taxpayers upto the amounts of difference between the excess tax payable (including-surcharge) on the income above Rs. 50 lakhs**/Rs.100 lakhs and the amount of income that exceeds Rs. 50 lakhs**/Rs. 100 lakhs respectively.

**Only for individual having income between Rs. 50 lakhs and below

Rs. 100 lakhs

Prominent deductions under Chapter VI-A for Non-Business Taxpayers:

(Subject to certain conditions as laid down in the Act/ Rule.)

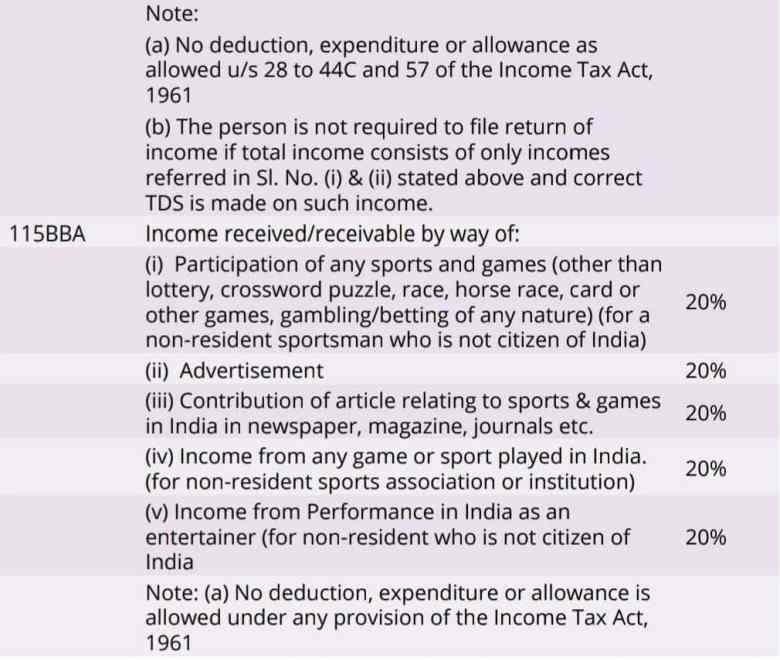

Special Tax Rates under Chapter XII

Special Tax Rates Under Chapter XII (Applicable to non-resident)

FILING of IT Return at

- Determine the types of IT Return required for you

- Registration on e-filing portal

- Aadhar linking with PAN

- Obtain Form 16/16A from Tax Deductor

- Check 26 AS for tax credit

- IFSC & Account no. of all bank accounts

- Registered e-mail id & mobile

- Generate e-verification code to avoid sending ITR-V, with the help of:

- Aadhar

- Registered Bank Account / ATM

- Net Banking

- Demat Account

- ATM/Debit Card or send ITR-V by post to CPC, Bengaluru

DIRECTORATE OF INCOME-TAX

(Public Relations, Publications & Publicity)

6th Floor, Mayur Bhawan, New Delhi