1) GST Amnesty Scheme 2021 2) Relaxation in Late – Fee Payment 3) Due Dates Extended 4) Other Relaxation

Summary of GST notification are tabulated below: –

| Relevant Notifications (Central Tax dated 01.05.2021) | |

| Notification No. Central Tax | Description |

| 08/2021 | Interest Relaxation for Tax Payable of Mar-Apr-21 |

| 09/2021 | Late Fee Relaxation for GSTR3B of Mar-Apr-21 |

| 10/2021 | Extension of GSTR-4 for FY 2020-21 |

| 11/2021 | Extension of filing ITC-04 for Q4 of FY 2020-21 |

| 12/2021 | Extension for GSTR-1 Due Dates for Apr-21 |

| 13/2021 | Relaxation for Rule 36(4) and furnishing IFF for Apr-21 |

| 14/2021 | Other relaxations for Completion or Compliance of Action under GST |

| Relevant Notifications (CT dated 01.06.2021) | |

| Notification No. Central Tax | Description |

| 16/2021 | Retrospective Amendment to Section-50 |

| 17/2021 | Due Date Extension GSTR1 for May’2021 |

| 18/2021 | Reduced ROI for Mar’21 to May’21 |

| 19/2021 | GST Amnesty Scheme and Rationalized Late Fees |

| 20/2021 | Rationalized Late Fees for GSTR1 |

| 21/2021 | Rationalized Late Fees for GSTR4 |

| 22/2021 | Rationalized Late Fees for GSTR7 |

| 23/2021 | Taxpayers Exempted from E-Invoicing |

| 24/2021 | Various Compliances Extended |

| 25/2021 | GSTR4 Extended for 2020-21 |

| 26/2021 | ITC04 for QE Mar’2021 Extended |

| 27/2021 | Extended IFF, Relaxations to Rule 36(4) |

INTEREST ON NET CASH BASIS

Section 50 of the CGST Act, 2017 which is also replicated in SGST Acts, contains the provision for levy of interest on delay or non-payment of GST.

In this regard, the Quantum of interest to be levied was under dispute from first day of introduction of GST.

The dispute was whether GST will be charged before adjusting ITC (on Gross Liability) or after adjusting ITC (Net Liability).

GST Council in its 43rd Meeting held that W.E.F 01.07.2017 – Retrospective amendment in section50 of the CGST Act, providing for payment of interest on net cash basis (after adjusting ITC) .

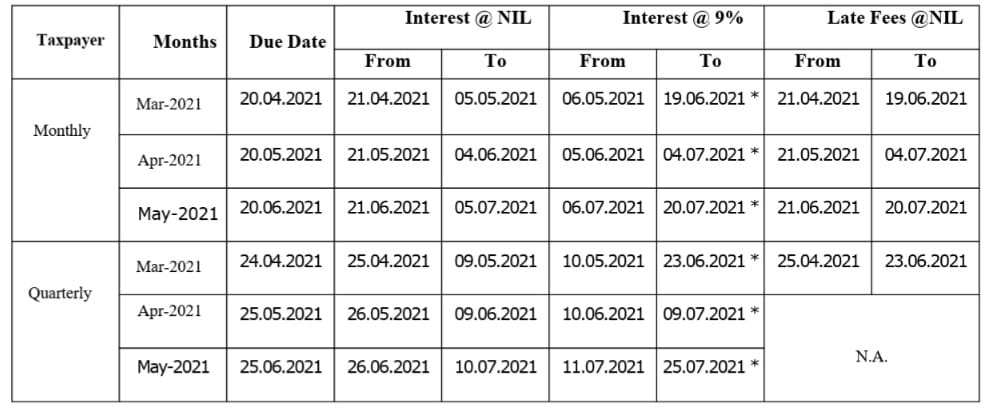

Interest Waiver as per Notification 08/2021 and relaxation as recommended by 43rd GST Council

For Turnover > 5 Crores in preceding FY in case of GSTR 3B Return.

For Turnover up to 5 Cr. in Preceding FY in case of GSTR 3B Return

CategoryAStates

For Turnover up to 5 Cr. in Preceding FY in case of GSTR 3B Return

Category BStates

Relaxations to Composition Taxpayers

Other Relaxations

- Due date for filing ITC04 (Goods dispatched to /received from Job work) for the Q4 (Jan-Mar) of 2020-21 has been extended to 30.06.

- Government Departments and local authorities are exempted from E-Invoicing provisions.

- Rule 36(4)pertain to restriction of ITC shall apply cumulatively for the period April, May and June 2021in the return FORM GSTR-3B for the tax period June-2021.

- The time limit for completion of action of verification by the proper officer of the application for GST registration and its approval (Rule-9 of CGST rules pertaining to Verification of the Application and Approval) falls between 01.05.2021 to 30.06.2021 has been extended to15.07.2021.

- Taxpayers registered under Companies Act can furnish returns by using EVC instead of DSC till 31.08.2021.

TIME LIMIT EXTENDED

Whose last dateofcompletionfallsbetween15thAprilto29thJuneisextendedto 30th June2021

1.Completion of any proceeding or passing of any order or issuance of any of the following:

1.Notice,Intimation,Notification

2.Sanction and Approval(by any authority, commission or tribunal)

2.Filing of any Appeal ,Reply and Application

3.Furnishing of any

1.Report

2.Document

3.Return

4.Statement or such other record

4. Refund Orders under Section 54(5) and Section 54(7) shall be extended up to

15 days after the receipt of reply to the notice

OR 30th June-2021 (W.E. later)

NO BENEFIT OF EXTENSION IN FOLLOWING THE SECTION

About the Author :

The author, CA Jayprakash Pandey is a practicing Chartered Accountant (Founder of Jayprakash P & Company) having Office at Mumbai, with more than 5 years of professional cum practical experience, Direct Tax, International Taxation, Indirect Tax & FEMA related advisory, litigation & compliance matters.

Disclaimer: The purpose of this is to share knowledge and it is for education purpose only. This does NOT constitute NOR does this form part of neither it is to be construed as, A LEGAL OPINION. The analysis is solely based on the reading abilities of the Author. They may be correct/incorrect as per you. No representation or warranty, express or implied, is made or given in respect of any information provided.

The author, CA Jayprakash Pandey is a practicing Chartered Accountant (Founder of Jayprakash P & Company) having Office at Mumbai, with more than 5 years of professional cum practical experience, Direct Tax, International Taxation, Indirect Tax & FEMA related advisory, litigation & compliance matters.