Introduction:

Net Present Value (NPV) is a fundamental concept in finance, serving as a cornerstone for investment appraisal and decision-making. It’s a powerful tool that allows businesses and investors to assess the profitability of an investment by considering the time value of money.

Understanding NPV:

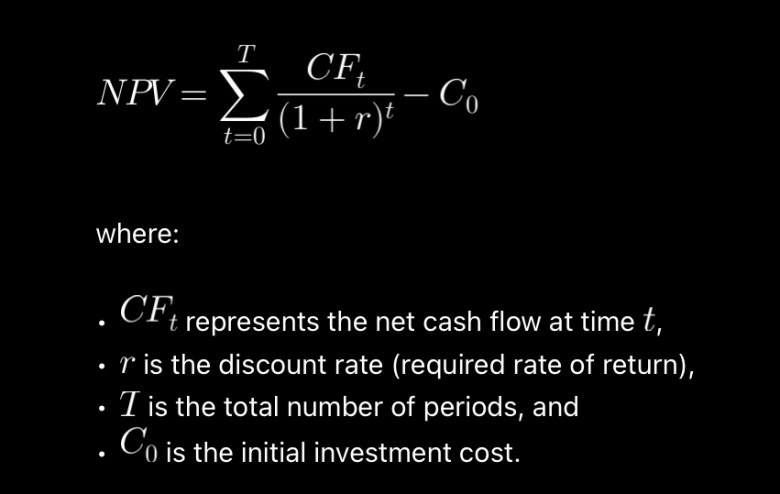

At its core, NPV involves calculating the present value of expected future cash flows generated by an investment and comparing it to the initial investment cost. The formula for NPV is:

Key Components of NPV:

- Discount Rate:

- The discount rate reflects the cost of capital or the minimum required rate of return. It considers the time value of money, acknowledging that a dollar today is worth more than a dollar in the future.

- Cash Flows:

- NPV is based on the expected cash inflows and outflows associated with an investment over its life. These cash flows can include revenues, operating expenses, and the eventual sale or salvage value.

- Initial Investment:

- The initial investment is the upfront cost required to undertake the investment. It includes capital expenditures, working capital changes, and any other costs associated with the project’s inception.

Interpretation of NPV:

- Positive NPV:

- A positive NPV implies that the present value of expected cash inflows exceeds the initial investment. This is an indicator that the investment is expected to generate value and contribute to shareholder wealth.

- Negative NPV:

- A negative NPV signals that the present value of cash inflows is insufficient to cover the initial investment. In such cases, the investment may not meet the required rate of return and could lead to a wealth reduction.

- Zero NPV:

- A zero NPV suggests that the investment is expected to yield exactly the required rate of return. While it doesn’t result in wealth creation, it at least meets the minimum performance expectations.

NPV in Decision-Making:

- Capital Budgeting:

- NPV is a crucial tool in capital budgeting decisions. It helps companies evaluate and prioritize potential projects or investments based on their contribution to shareholder value.

- Comparative Analysis:

- When faced with multiple investment opportunities, NPV allows for a comparative analysis. By comparing the NPVs of different projects, decision-makers can choose the most financially attractive option.

- Risk Consideration:

- NPV can be adjusted to incorporate risk by using a risk-adjusted discount rate. This helps account for uncertainties in cash flow projections and provides a more realistic assessment of an investment’s viability.

Challenges and Considerations:

- Assumptions and Projections:

- NPV relies on accurate cash flow projections and discount rate assumptions. Variability in these factors can impact the reliability of the NPV calculation.

- Time Horizon:

- The choice of the investment’s time horizon influences NPV results. Shorter timeframes might neglect long-term benefits, while overly extended periods can introduce uncertainty.

- Changing Discount Rates:

- Changes in the discount rate over time can affect NPV. It’s crucial to consider the stability of the discount rate or apply sensitivity analysis to assess the impact of rate variations.

Conclusion:

In conclusion, Net Present Value stands as a paramount metric in financial decision-making. Its ability to incorporate the time value of money, assess profitability, and guide capital allocation makes it an invaluable tool for businesses and investors alike. Despite its power, the accuracy of NPV depends on the quality of assumptions and projections. Therefore, a thoughtful and well-informed approach is essential when utilizing NPV for investment appraisal and strategic decision-making.